The Economic and Fiscal Impacts of Restricting Housing Growth in the City of Lakewood, Colorado

Primary Author: Chris Brown

In Partnership with Common Sense Policy Roundtable, Colorado Association of REALTORS®, Colorado Concern, Denver South Economic Development Partnership

About the REMI Partnership

A partnership of public and private organizations announced in July 2013 the formation of a collaboration to provide Colorado lawmakers, policy makers, business leaders, and citizens, with greater insight into the economic impact of public policy decisions that face the state and surrounding regions. The parties involved include the Common Sense Policy Roundtable, the Colorado Association of REALTORS, Colorado Concern and the Denver South Economic Development Partnership. This consortium meets monthly to discuss pressing economic issues impacting the state and to prioritize and manage its independent research efforts.

Acknowledgements

We would like to acknowledge and give a special thanks to Deborah Shipley with REcolorado, and Tom Hayden with Metrostudy for their expertise and efforts to provide the most credible and accurate regional data used as part of this research effort. Also, thank you to Tyler Brown of AMG National Trust Bank, for advice on how to analyze the issue and significant contributions to editing the final report.

Executive Summary

In a period of rapid-growth and prosperity, a central question facing Coloradans is, “How do we manage anticipated growth?”

Maintaining the quality of life that defines the Colorado experience should be a top priority for elected officials and residents. The availability and affordability of homes is critical for individuals to raise a family, start a career and generate wealth. Businesses also need to be able to continue to attract and retain talented workers that can afford to live and thrive in the communities they work. Comprehensive city plans, created through citizen input, help to establish zoning that take these factors into account and outline how development in a community can proceed.

“Building Gated Cities”

Building Gated Cities takes an in-depth look at a proposed 1% housing growth limitation in the City of Lakewood and the potential social and economic impacts of the measure. The initiative serves as a case study for a larger debate over policies to address sustainable growth.

Research suggests the “1% growth” initiative in the City of Lakewood works directly against its own stated interests, and the interests of the region, as over the next decade it forces up to 4,000 households to locate elsewhere in the metro area. A recent draft study released by the city of Lakewood found there are already significant pressures on the Lakewood housing market:

- Median home prices are already beyond what a growing share of local workers can afford, including police and firemen on a single salary.

- The city has grown primarily in the areas where growth was designated in the city’s comprehensive plan, and can afford to add density and growth in the areas zoned for it without impacting the quality of existing residential areas.

Report Findings

This report builds on the city’s findings to suggest that the proposed legislation to limit housing growth in Lakewood, which is intended to cut down on congestion and improve quality of life, is actually likely to achieve the opposite.

Major findings of the study include:

- The pending 1% growth initiative proposed in the City of Lakewood would have significant impacts on the city’s future and jeopardize the issues residents care about the most.

- As indicated in recent surveys, the items that citizens of Lakewood deem most important – affordable homes, access to a range of amenities, and less traffic congestion – are directly at odds with the proposed initiative.

- Estimates suggest the measure could reduce the projected number of households in Lakewood by 10% to 18% over the next 10 years.

- The reduction in housing availability will likely drive up the cost of living, contribute to widening income inequality, increase congestion and urban sprawl, and reduce the local consumer base that draws in desirable retail options.

- Along with the upward pressure on housing costs, over the next decade the city could forgo up to $1.046 billion in residential construction investment and up to $263 million in household disposable income that could have gone to supporting local businesses.

- The 1 % growth initiative will also leave Lakewood’s major public infrastructure investment, the West Rail Line, challenged to realize its potential by preventing denser housing growth in the areas surrounding rail stops.

Study Conclusion

The City of Lakewood has a responsible plan to manage growth that has been developed through ongoing efforts to involve input from the community. The Lakewood 1% growth initiative, and other growthlimiting initiatives like it, directly oppose city and regional efforts to follow growth plans that allow for healthy and sustainable development. When choosing how to manage anticipated growth, our region needs policy that allows for markets to respond to demand for housing, and to meet the desires of both current and future generations.

Colorado Growth

- Colorado’s economy has grown rapidly in recent years, leading to strong demand for new housing

- Cities and the regional planning authorities have created detailed, comprehensive zoning plans by engaging with local citizens

- Proper zoning allows for growth in the number of households without sacrificing the vision for the community as a whole

The recent history of Colorado and its major metropolitan areas is a story of growth. Fueled by a strong job market, relative affordability, and unique access to the outdoors, thousands of individuals and families have decided to make Colorado home in recent years. However, the rapid growth has also put a strain on Denver and its surrounding metro areas, illuminating the need for strong leadership and community engagement. How Colorado citizens and lawmakers choose to address the state’s growth is one of the largest questions facing policymakers today.

Cities across the Front Range have engaged with citizens and collaborated with regional organizations to design comprehensive zoning plans that merge the demands of the community with the realities of the future. While no plan is perfect, these efforts have allowed for open dialogue and have given communities a voice in the process. Through the zoning process, cities strive to achieve the goals and vision established through a comprehensive regional plan, while the needs of businesses and households drive the physical development of commercial and residential structures.

Concerns surrounding growth in Colorado have led some to assume that the solution is to simply restrict the construction of new homes. In the city of Lakewood specifically, there is a pending ballot initiative that caps the number of new residential permits that can be granted in any given year to no more than 1% of the existing housing supply. As the average number of new households in Lakewood has been growing at around 1.6% per year, this measure would severely restrict Lakewood’s housing supply relative to demand, which could lead to lower construction demand, lower household incomes and more upward pressure on home prices. Unfortunately, the restriction of housing supply in Lakewood will only exacerbate housing affordability issues for middle-class workers, who have already seen growth in home prices far outpace their income in recent years.

Table 1: Growth in Median Household Income vs Median Home Prices (nominal change)

In this report we discuss existing mechanisms to plan for growth in the Denver metro area, provide an outline of the proposed Lakewood 1% growth ballot measure, and estimate a range of economic impacts that could occur if the initiative were to pass.

Planning for Growth

DRCOG Vision

- The Denver Metro regional vision allows for strong growth in employment and population, largely by focusing growth in dense urban areas along transit corridors

- The Metro Vision aims to increase the share of housing in urban areas from 10% to 25% and the share of employment in urban areas from 36% to 50% by 2040

- The Vision strives to preserve the way of life for most communities and create an additional 14% of open space

Each city is ultimately responsible for establishing its own plan for development; however, the Metro Vision (Denver Region Council of Governments, 2017) plan adopted in January 2017 by the Denver Region Council of Governments (DRCOG) presents clear and actionable insights into how the region could grow while maintaining quality of life and affordability. DRCOG is a diverse organization that serves as the area’s metropolitan planning organization, the federally-designated Area Agency on Aging, the Council of Governments, and the Regional Planning Commission. As the Council of Governments, they provide technical assistance and coordination among local elected leaders, and as the Regional Planning Commission they prepare the plan for the physical development of the region. Primary goals of the regional plan include:

- An efficient and predictable development pattern

- The creation of a connected multi-modal region

- Safe and resilient natural and man-made environments

- Healthy, inclusive and livable communities

- A vibrant regional economy

These aspirational goals are met through a detailed examination of both developed and undeveloped land. Related to housing, the Metro Vision establishes several core themes that should drive decisions around future residential growth:

- New urban development occurs in an orderly and compact pattern through regionally-designated areas

- Connected urban centers and multimodal corridors throughout the region accommodate a growing share of the region’s housing and employment

- Diverse housing options meet the needs of residents of all ages, incomes and abilities

As of 2014, 10% of Denver metro area housing was in areas designated as urban centers and 1.2% of housing was in areas at higher risk for natural and human caused hazards. The Metro Vision aims to increase the share of housing in urban centers to 25% and decrease the share of housing in high-risk areas to less than 1% by 2040. By allowing development to occur in this manner, the region will be able to preserve an additional 14% or 259 square miles of protected parks and open space.

Lakewood Housing and Comprehensive Planning

- “Lakewood 2025: Moving Forward Together” is the city’s adopted comprehensive plan that establishes the zoning restrictions within city limits

- A recent study found the city has added residential units in the areas identified within the plan, and can accommodate higher density growth in designated areas without impacting the character of the community

- Housing affordability in Lakewood is already at a breaking point, with civil servants such as firemen and police challenged to afford to live in the community they serve

The existing efforts by the City of Lakewood and its citizens to address future growth led to the creation of “Lakewood 2025: Moving Forward Together,” (City of Lakewood, April 2014) a comprehensive plan for the growth of the city. The plan was crafted through open houses and direct input from members of the community. In 2014 a Comprehensive Plan Advisory Committee was formed and met 17 times, with each meeting open to the public. The Advisory Committee consisted of two resident representatives of each City Council ward, one representative from each business association within the city, and professional staff from the City Planning Commission. In February 2015, the draft plan was presented at two community open houses, and through drop-in office hours held for those that could not attend. In March 2015, a public hearing before the Planning Commission heard comments and approved the plan, and in April 2015 the Lakewood City Council approved the plan.

A recent study (Economic & Planning Systems, Inc. and RRC Associates, August 28, 2017) provides an in-depth look at the current housing situation in Lakewood. The report looks at the existing housing market from both the demand side and supply side. Through a survey it also discusses stated housing preferences of the local population and provides insight into how well the city’s residential landscape is meeting those expectations.

Summary of Lakewood Housing Study’s purpose and key findings:

- Research seeks to underscore the connection between economic development, the growth of the city’s economy, and the availability of diverse housing options

- Meeting future demand is more than just adding an adequate number of units; it also means providing the associated amenities that residents of all ages desire, such as close access to shopping, dining, recreational space and transit options

- Population growth has not kept pace with employment growth in the city and number of incommuters climbed from 9% of workforce to 17% from 2002 to 2014

- The city only added one housing unit for every three jobs between 2000 and 2015 compared to the 5-county Denver-Aurora-Lakewood metropolitan statistical area average of nearly one unit for every job

- The supply constraint on housing will eventually cause prices to rise beyond what even the city’s essential civil servants can afford. In 2015 the median home price in Lakewood was an estimated $66,000 and $98,000 more than a starting police officer or West Metro firefighter could afford on a single salary. By 2016 that gap between what a police office and firefighter could afford grew to $107,000 and $139,000, respectively

- The city has facilitated most of its high-density residential growth in areas designated for growth within the comprehensive plan

- The city has limited space to facilitate additional growth except infill sites, redevelopment opportunities and a few areas for new development

- The city could increase its housing density in areas designated within the Comprehensive Plan without disturbing or altering the character of the community

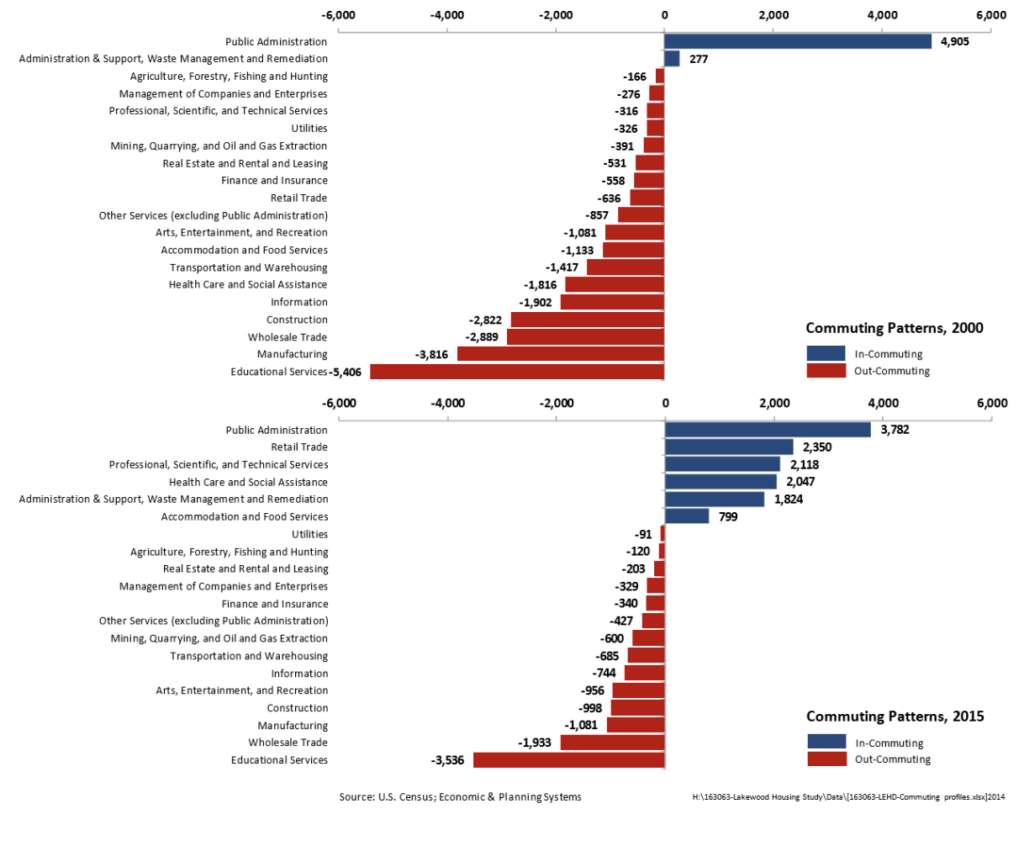

Some of the most telling findings are related to a widening gap in the type of workers that can afford homes within the city of Lakewood. Figure 1 shows the growing share of the Lakewood workforce by sector that commutes into the city. In 2002 the only industry that saw net in-commuters was public administration. In 2014 that list of sectors also included retail trade, professional, scientific and technical services, health care and social assistance, administration and support, waste management and remediation and accommodation and food services.

Figure 1: Commuting Patterns, 2002-2014 (Economic & Planning Systems, Inc. and RRC Associates, August 28, 2017)

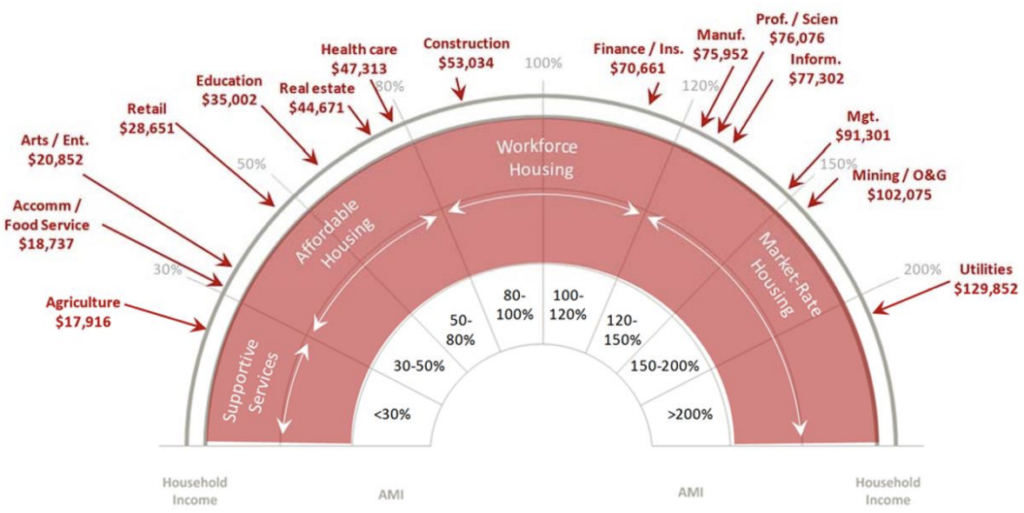

The study also gives some insight into the earnings needed to afford a median home within the city. Figure 2 shows what type of home would be affordable for different wage earners, assuming a household with one income earner.

Figure 2: Household income levels with individual wage associations (Economic & Planning Systems, Inc. and RRC Associates, August 28, 2017)

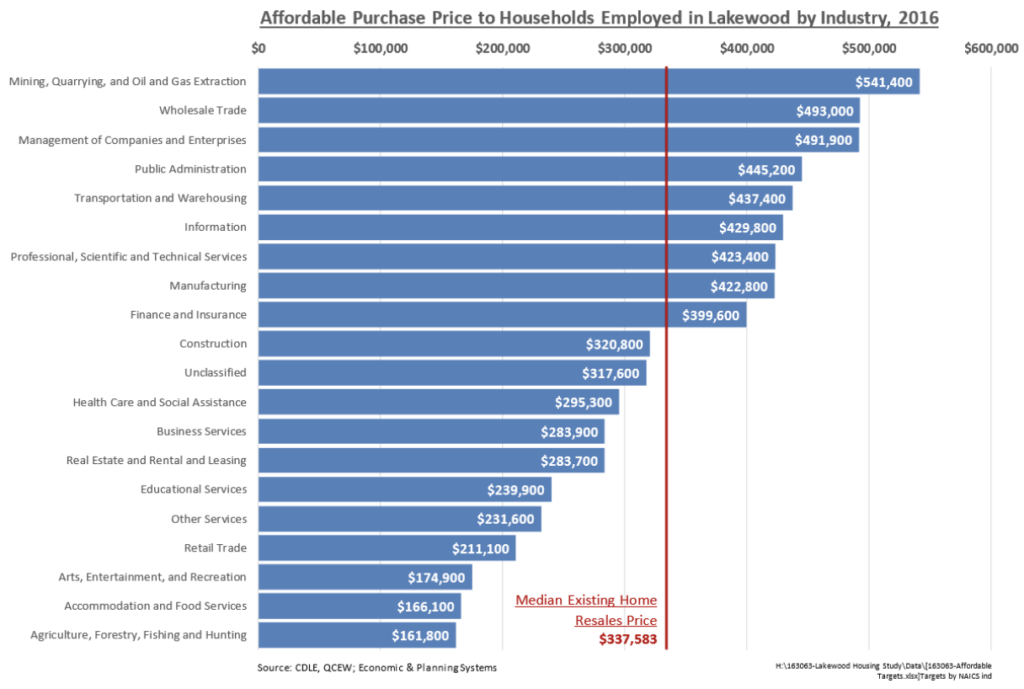

By estimating the affordable home price by sector using weighted household income, the study also looked at which employment sectors pay enough to allow a worker to afford the 2016 Lakewood median home price (Figure 3). The sectors in which workers cannot afford the median price home represent roughly 62% of Lakewood’s total employment (Lakewood Economic Development, City of Lakewood, 2017).

Figure 3: Target purchase price of homes, based on estimated weighted sector averages (Economic & Planning Systems, Inc. and RRC Associates, August 28, 2017)

Lakewood ‘1% Growth’ Initiative

- Would establish a new governmental council to administer a system that provides permit allocations to prospective residential developers

- The exact number of units allowed for development would be established the year prior but would equal no more than 1% of the existing number of units

- An arbitrary cap of 1% growth on new residential units would undermine the ability of the city and the region to properly grow while further impacting affordability throughout the region

The Metro Vision and city comprehensive plan can only be implemented if growth is allowed to proceed in a smart and flexible manner. The proposed 1% growth ballot measure will ask residents to consider an entirely different strategy to address growth. Arbitrarily restricting residential growth to 1% per year, and placing a cap on the number of new housing units that can be permitted, threatens Lakewood’s vision to allow for increased affordability and economic health.

The proposed ballot measure is not a new strategy, and similar growth restrictions already exist in the nearby cities of Golden and Boulder, where the median home prices for 2017 so far are $521,000 and $637,187- or about 49% and 82% higher, respectively, than the median price in the city of Lakewood.

Key aspects of the 1% growth ballot measure:

- Requires anyone seeking to obtain a residential building permit to first seek an “allocation” from a yet to be determined newly established group within the city

- The number of allocations would be set each year to equal 1% of the previous year’s total estimated housing units

- “Allocations” would be divided into pools based on the type and desire for obtaining a residential building permit

- Open pool

- Hardship pool

- Affordable/low income housing pool

- Surplus pool

- Certain new residential units would be exempted from cap

- Housing for higher education

- Housing on “blighted” land

- Upon some additional approval, age 55 and over only communities

- Measure further restricts multi-family developments seeking permits for more than 40 units in any given year to seek additional approval

- Allows applicants to apply for more permits than available in any given year and to “bank” those allocations to receive permits in following years

Growth restriction opposes city and regional visions and the citizens of Lakewood

Through a survey of over 1,344 Lakewood workers, the Lakewood Housing Study also provides insight into what the citizens of Lakewood want their community to look like. One underlying theme is the desire to have walking proximity to amenities such as restaurants, retail and grocery stores, as well as public transit options. These views are core themes to the regional Metro Vision, which argues that people living in proximity to work, shopping and transit reduces infrastructure costs and helps keep congestion manageable.

Figure 4: Areas in Lakewood within walking distance to employment centers (Economic & Planning Systems, Inc. and RRC Associates, August 28, 2017)

![]()

Figure 5: Areas in Lakewood within walking distance to retail and redevelopment (Economic & Planning Systems, Inc. and RRC Associates, August 28, 2017)

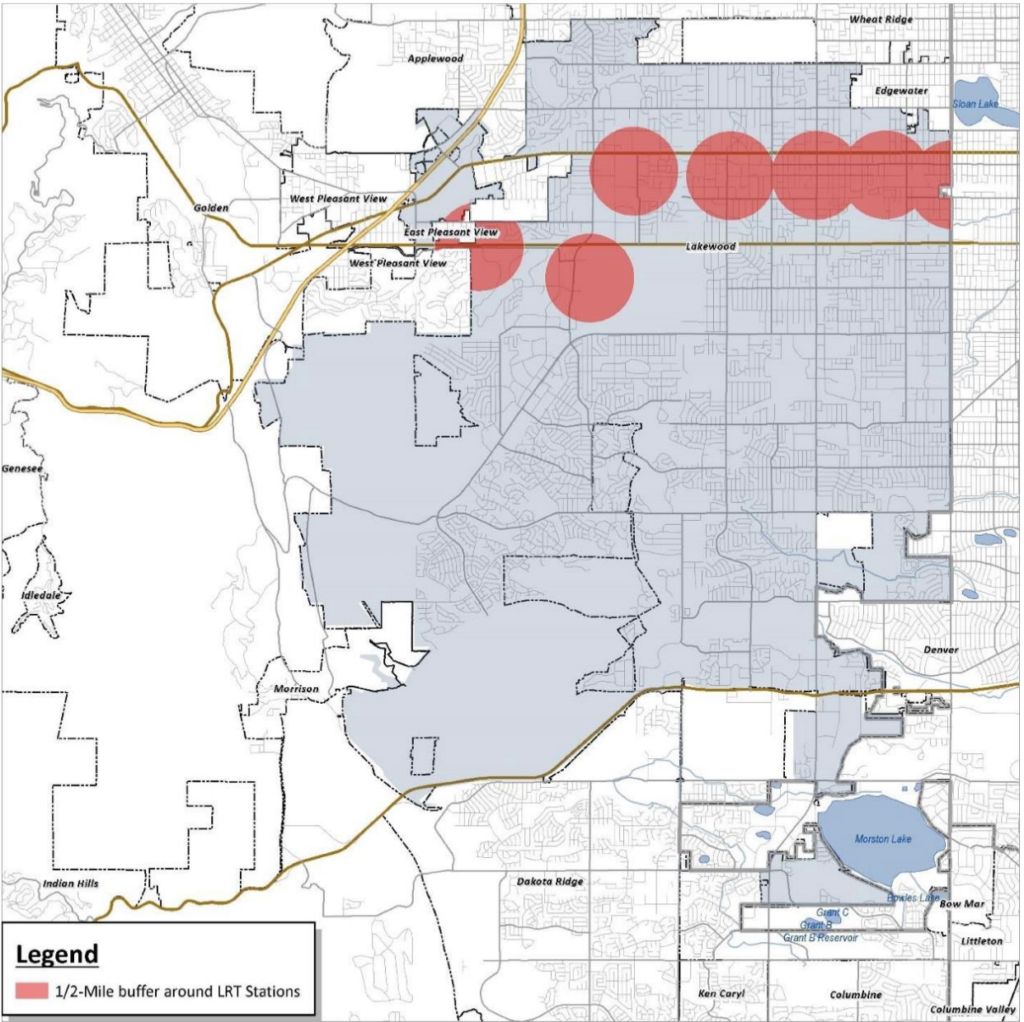

Figure 6: Areas in Lakewood within walking distance to fixed rail transit (Economic & Planning Systems, Inc. and RRC Associates, August 28, 2017)

The City of Lakewood’s comprehensive plan expects much of the area’s growth to center around areas that are within walking distance to the West Rail Line running along the north part of the city. In public forums in 2011, when discussing the plans to complete the 12.1-mile portion that runs through the city, the Mayor and the City Manager at the time stressed how Lakewood was one of the cities in metro Denver most prepared to accommodate transit-oriented development. Given that much of the growth along that rail line would need to be larger multi-family units, any effort to cut the size and number of residential units would undermine the established goals of the city plan.

Figure 7: Growth Areas Targeted In Lakewood Comprehensive Plan (Economic & Planning Systems, Inc. and RRC Associates, August 28, 2017)

![]()

Residential permit data shows that the average number of new housing permits given out in Lakewood over the past three years was 870, though it rose as high as 1,190 in 2014 and fell as low as 652 in 2015. The large annual fluctuations are to be expected given the way the financing, engineering, and construction of large multi-family units occur. Under the new 1% growth initiative, this flexibility would be limited. Further, there is the possibility that developers of buildings containing more than 40 units would be granted only some of the necessary permits, and would be unable to complete the development until they could get the remaining permits in later years. Such a dynamic would undoubtedly increase the uncertainty to developers and could make it more difficult for developers to obtain financing for multi-unit projects- the projects that are most needed to ensure sufficient housing density and affordability.

The stated purpose of the 1% growth initiative is a preference to avoid degradation in air and water quality, and to ensure that growth does not exceed the availability of public facilities and urban services. While it is not entirely clear what facilities or services are being referenced in the proposed initiative, forcing growth in less-dense housing generally results in higher per-unit costs and tends to place added stress on local roadways, utilities, and water services. Thus, the 1% growth initiative may actually end up doing the opposite of what it intended by putting more strain on local infrastructure.

Further, the city’s comprehensive plan targets higher-density, mixed use development that will allow for lower-income workers to live in the communities they work, which would not only alleviate some of the pressures on existing roads, but could solve other problems as well. For example, in guidance issued by the US EPA (Kevin Nelson, 2009), one of the proposed solutions for mediating environmental risks is to increase housing density in city centers. According to the guidance, promoting responsible housing density in these centers has a variety of benefits, including protecting outlying open spaces and sensitive habitats, increasing energy efficiency, and protecting water quality.

The citizens of Lakewood should be aware of the city’s existing growth management strategy and should be informed about the potential societal and economic impacts of diverting from that strategy by capping residential housing permits in the manner suggested by the 1% growth ballot measure.

Economic Impacts of Restricting Residential Growth

- Under a 1% residential growth cap, the city of Lakewood could forgo between $276,201,568 and $1,045,809,080 in residential construction investment and $69,558,012 and $263,450,171 in local consumer spending over the next decade

Through work conducted earlier in 2017 (Common Sense Policy Roundtable, 2017), we discussed the strong connection between rising home prices and slower economic growth. The resale market for existing lower value homes in the Denver metro area has steadily outpaced new construction in recent years, particularly in the area of condominiums. At a time when the decline in vacancy rates is bottoming out and demand is expected to continue growing, further restriction of housing supply in the Denver metro and surrounding areas would only exacerbate the problem of unaffordable home prices.

As discussed in earlier sections, the supply of adequate and affordable housing is a vital component to a regional economy. The availability of affordable housing is critical to retaining a skilled workforce, keeping local business competitive, and reducing urban sprawl. It also gives young people the chance to purchase rather than rent, allowing them to begin building valuable home equity. Conversely, a lack of affordable housing near employment centers pushes workers farther from their jobs, forcing them to commute longer distances, putting undue strain on local roadways and public transportation, and dis-incentivizing workers and their employers to locate in the area.

Simulating Dynamic Economic Impacts

To estimate the economic impacts of the proposed ballot measure on the City of Lakewood, we use the dynamic economic model PI+ developed by Regional Economic Models, Inc. (REMI), which is customized to track the impacts of new policies on state and local economies. We project the economic “shock” from the proposed ballot measure by observing its potential impacts on key supply and demand measures:

- Demand Impacts

a. Forgone residential investments b. Lower household spending on local services and businesses - Supply Impacts

a. Increase in home and rental prices

REMI PI+ is used throughout the country by state, local, and private organizations to aid in the development of public policy. The model used in this study is a customized 3-region model including Metro Denver, Denver South and the rest of the state. For the results, we combined Metro Denver and Denver South to a single 7-county region. Those counties include Adams, Boulder, Broomfield, Denver, Jefferson, Arapahoe, and Douglas. The direct changes that occur in the city of Lakewood as a result of the 1% growth initiative are extrapolated to simulate the dynamic impact on this greater region.

Establishing the Baseline

- Lakewood “Strategic Growth Initiative” establishes a starting point of 67,220 units, allowing for 672 units to be developed in 2018 under the 1% growth policy

- To determine the projected housing demand, we use two different sources:

- The city comprehensive plan, which cites DRCOG saying the city needs an average of 812 units to be built annually

- Lakewood’s share of Jefferson County’s growth, which has averaged 34% in recent years; if this trend continues, 1,086 units would be needed to keep pace with the expected growth of the county

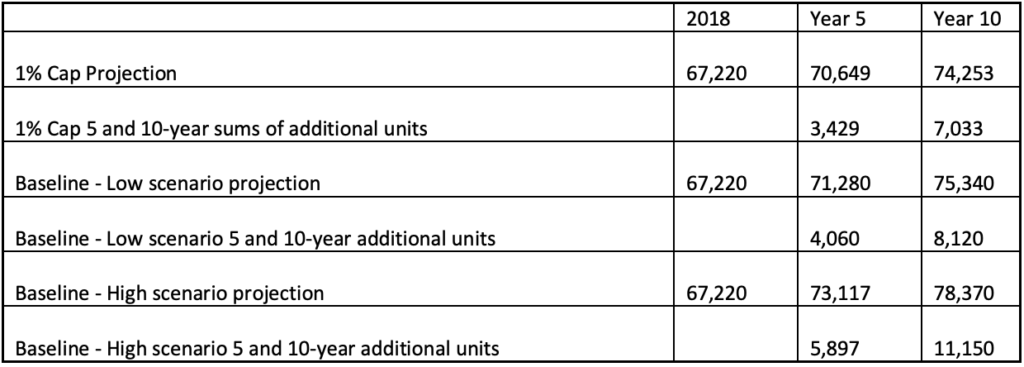

To determine the potential range of impacts from the proposed ballot measure, first it is necessary to establish what residential growth would look like in the future under current policy compared to what it would look like with a 1% cap. As a starting point, for 2018, we chose to take the estimate provided within the “Strategic Growth Initiative Ballot Language and Ordinance” under its discussion of available allocations. The proposed legislation’s estimate was developed using a 5-year average of people per housing unit for the City of Lakewood. Dividing the population estimate from the City’s 2017 Community Profile by the number of people per household, 2.27, we arrive at a base estimate of 67,220 housing units, with an allowed 1% growth of 672 units for 2018.

We then compare this amount to what we estimate the actual demand for housing growth in Lakewood may be in the future. From within the City’s Comprehensive Plan, there is an estimated 812 units needed on average over the next decade to meet expected demand. This figure uses an average household size of 2.32 people per household, a bit higher than recent average levels (see 2.27 above) and higher than would be expected in the future as average household sizes continue to decline. Thus, in our simulation we use the city’s estimate of 812 units demanded each year as a conservative lower bound.

Another way to gauge the potential demand for new households is to estimate the city’s share of projected county-level growth. The five-year average of Lakewood’s share of larger Jefferson County’s household growth is 34%. Applying this share to the projected growth in households for the county, we get an annual average of 1,086 units needed over the next decade. The simulation uses this demand estimate as an upper bound.

The table below shows expected annual growth in housing units under the two demand scenarios, versus the proposed 1% cap. The ballot measure discusses how the housing cap will be estimated in each year, which can include consideration of any annexed or destroyed units that are not replaced; however, given the uncertainty around such estimates, we use the base capped rate of 1%.

Table 2: City projected housing demand with and without 1% growth cap

Table 3: High and Low scenario – Forgone residential housing units

After determining the projected difference in housing units from what would be expected under current policy, we can then develop scenarios to estimate the dynamic impacts on the regional economy.

Demand Impacts

Using data sourced from several local developers, in collaboration with Metro Study, a rough estimate of Lakewood’s average per-unit cost of construction excluding land is $321,750 for a single-family detached home and $225,000 for all others. Therefore, against our current high and low baselines, the 1% cap would reduce residential construction investment in the city between $276,201,568 and $1,045,809,080 over the next 10 years.

Residential construction spending supports local job growth through the hiring of contractors, architects, engineers, and construction workers, among other diverse services and suppliers. The vital supply chain of residential construction is well-documented, and estimates compiled from the national GDP accounts by the National Association of Homebuilders indicate that the residential construction market, including renovations, contributes roughly 13%-15% of total U.S. Gross Domestic Product (GDP). Thus, the loss of direct investment in residential real estate can have far-reaching negative impacts on the economy.

Along with the loss of direct investment, the city also forgoes the disposable income that displaced households could have retained and spent in the area. Simulations suggest the 1% growth initiative could reduce household disposable incomes in Lakewood between $69,558,012 and $263,450,171 over the next ten years.

As a large part of household spending tends to go to local businesses, the region will also forgo a significant amount of local consumption that would otherwise have gone to the same businesses and service providers Lakewood citizens identified as important in the city’s housing study, such as retail stores, restaurants, and medical providers.

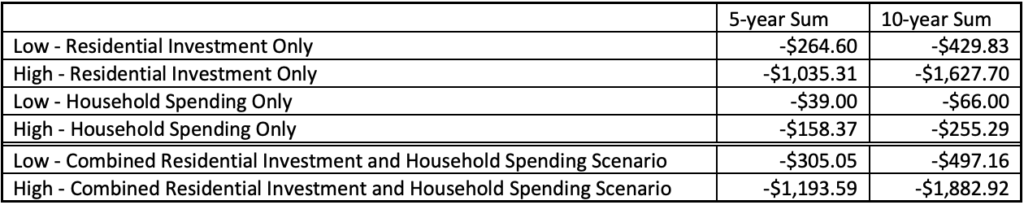

The tables below show the 5 and 10-year estimates for direct losses to residential investment and household spending.

Table 4: Lakewood direct loss in residential investment spending (fixed 2017$)

Table 5: Lakewood direct loss in residential household spending (fixed 2017$)

As a result of a direct loss in residential construction investment, there will be significant downstream impacts to the broader economy through the loss of intermediate demand and local consumption demand. In the case of the Lakewood growth restriction, it may be that while the city itself will experience significant direct losses, the larger metro area and the state could retain some construction and spending activity because households are able to relocate elsewhere in the region. The ability for the metro region outside of Lakewood to take on a larger share of growth should be studied further, but as previous findings suggest (Rosenthal, 2005), the additional supply pressure in the housing market will likely force home prices to increase. This issue is discussed further in the next section. The following tables estimate dynamic economic impacts to the 7-county region from lower direct residential construction and household expenditures, under the assumption that the region loses out completely on the slower residential growth in Lakewood. The results present impacts to both GDP and Jobs figures. Both include the full range of industries across the region and represent the cascading impacts as reductions in expenditures ripple through the economy.

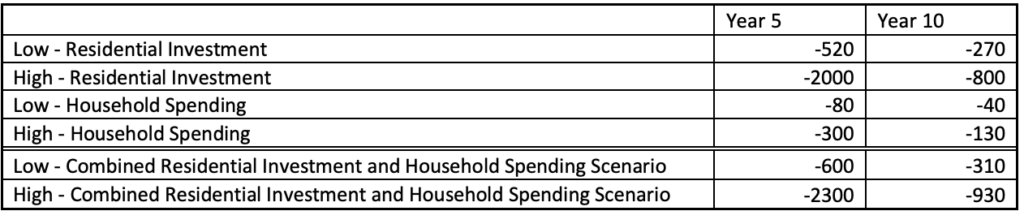

Table 6: GDP Impacts of lower residential investment and household spending (fixed 2017$ Millions)

Table 7: Jobs impacts of lower residential investment and household spending

Supply Impacts

Over the past 10 years, the median home price in the City of Lakewood has grown at 6.4% annually, while in the Denver metro area prices have grown at 5.8%. In just the past five years those figures have jumped to 12.2% and 10.3% respectively.

Lakewood median prices have also grown faster than those of the larger region, increasing 83% since 2010 versus the region at 77%. At the same time, nominal growth in household incomes has only been 44% in the region over the same period. With housing costs dramatically outpacing income growth, a measure like the 1% growth initiative that could force 4,100 potential households out of Lakewood may only make the situation worse.

Further, in the last five years detached median home prices in Lakewood have grown an average of 11.4%, while prices of attached homes have grown 16.4%. This suggests strong demand or under-supply specifically for attached, multi-unit properties. Thus, a self-imposed cap on new units in the Lakewood area, particularly one that discourages multi-unit construction, will only make it harder for housing supply to meet demand.

In our previous analysis of housing affordability in the Denver area, we found that even a 1% increase in the cost of housing would result in metro area citizens losing roughly $239 million dollars in real disposable income. Higher housing costs crowd out other spending, resulting in ripple effects across the economy, but have a particularly severe impact on fundamental sectors like retail and healthcare. Higher housing prices also slow the number of people and companies willing to move to the region.

Fiscal Impacts

Beyond the impacts felt through the economy on employment and income growth, the city and region will also face various fiscal and budgetary impacts. Even if all the households that can no longer live in Lakewood are able to find a new home in another part of the region, the City of Lakewood will inevitably lose out on valuable tax revenue.

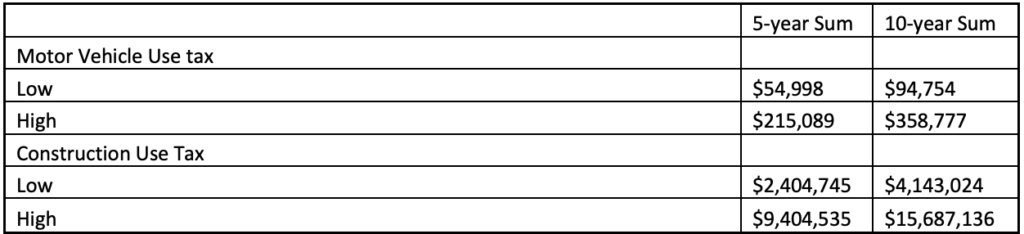

With less residential investment and lower consumer spending, the city will collect less revenue related to permitting and developing new homes. Based on figures in Lakewood’s 2016 financial report (Department of Finance, City of Lakewood, Colorado , 2017), construction and motor vehicle-related use taxes have become an important source for the city’s General Fund. Given our projections on the reduced number of homes that would be built under a 1% permitting cap, the city could lose between $4,100,000 and $15,700,000 in construction use taxes alone over the next ten years.

Table 8: Lower construction and motor vehicle use tax revenue (fixed 2017$)

Lakewood would also forgo revenue growth from the cumulative loss in new households, due to lower revenue from general use and sales taxes. The city’s financial report estimates that it had $2,600,000,000 in taxable sales in 2016. At an assumed average use tax rate of 3%, the city would have collected roughly $78,000,000 from taxable consumption, or about two-thirds of all Lakewood taxes collected. By crowding out households and businesses, Lakewood would be limiting a key source of its fiscal revenue.

Property taxes

Under a 1% cap, as residential home prices increase and the relative number of residential units declines, there will be a combination of factors that lead to a change in property taxes paid by homeowners. Existing laws in the state restrict the amount of additional property taxes that can be collected year-to-year. They also establish how much of the revenue collected is to come from residential properties versus commercial properties. As the city sees a decrease in the number of housing units relative to other parts of the region, several impacts could result:

- Existing homes will pay a higher share of taxes

- City will lose property tax collected directly by the city

- Should families relocate their children outside of Lakewood school districts, Lakewood will see less money come in from the county

- Other county services that operate in the city, such as sheriffs and courts, will be cut back

If we use current assessment rates, mill rates, and home values, we can come up with a general estimate of the amount of forgone tax revenue to both the city and county:

Table 9 – Lower property tax revenue (all property taxes, county average mill rate, fixed 2017$)

As home values and assessed values rise the amount each homeowner pays in property taxes will also increase. Should the rate at which home values increase outpace the cap in revenue allowed under state law, existing homeowners will have to pay a larger share of property taxes.

Conclusion

The pending 1% growth initiative in the city of Lakewood dictates a starkly different and in many ways more negative future for the residents of Lakewood than would otherwise be the case. The initiative also stands in contrast to established city and regional plans that strive to balance the interests of current residents with the needs of future growth.

As indicated in recent surveys, the items that citizens of Lakewood deem most important- affordable homes, access to a range of amenities, and less traffic congestion- are directly at odds with the proposed initiative. Estimates suggest the measure could reduce the number of households in Lakewood by between 13% and 18% over the next 10 years, which will likely drive up the cost of living, increase income inequality, contribute to greater congestion and urban sprawl, and reduce the local consumer base that draws in desirable retail options. The 1% growth initiative will also likely leave Lakewood’s major public infrastructure investment, the West Rail Line, unable to realize its desired potential by preventing denser growth in the immediate areas surrounding rail stops.

Those that currently own homes in Lakewood may see the value of their properties increase, but any decision to further restrict housing growth will infringe on the ability of others to share in that prosperity, and will negatively impact the larger societal and economic health of the community.

The future of the Colorado economy and the economic well-being of the people that live here depend upon having a market that can respond to demand. When proposed legislation restricts an area’s ability to grow, voters and policymakers should be aware of potential socioeconomic consequences that could undermine many of their own interests.

Download the Full Study and Executive Summary in pdf format >>